Cardiology Diagnostics Market Expansion Anchored by North American Dominance and Asia-Pacific Growth

The global cardiology diagnostics market is projected to grow at a significant compound annual growth rate (CAGR) during the forecast period from 2024 to 2031. This growth is driven by increasing prevalence of cardiovascular diseases, advancements in diagnostic technologies, and rising demand for early and accurate diagnosis.

Download Sample PDF:

Market Overview

Cardiology diagnostics encompass a range of tests and procedures used to diagnose and monitor heart-related conditions. These include imaging techniques, electrocardiograms (ECGs), stress tests, and biomarker assays. The market is experiencing growth due to factors such as an aging population, lifestyle changes leading to heart diseases, and technological innovations in diagnostic tools.

Market Segmentation

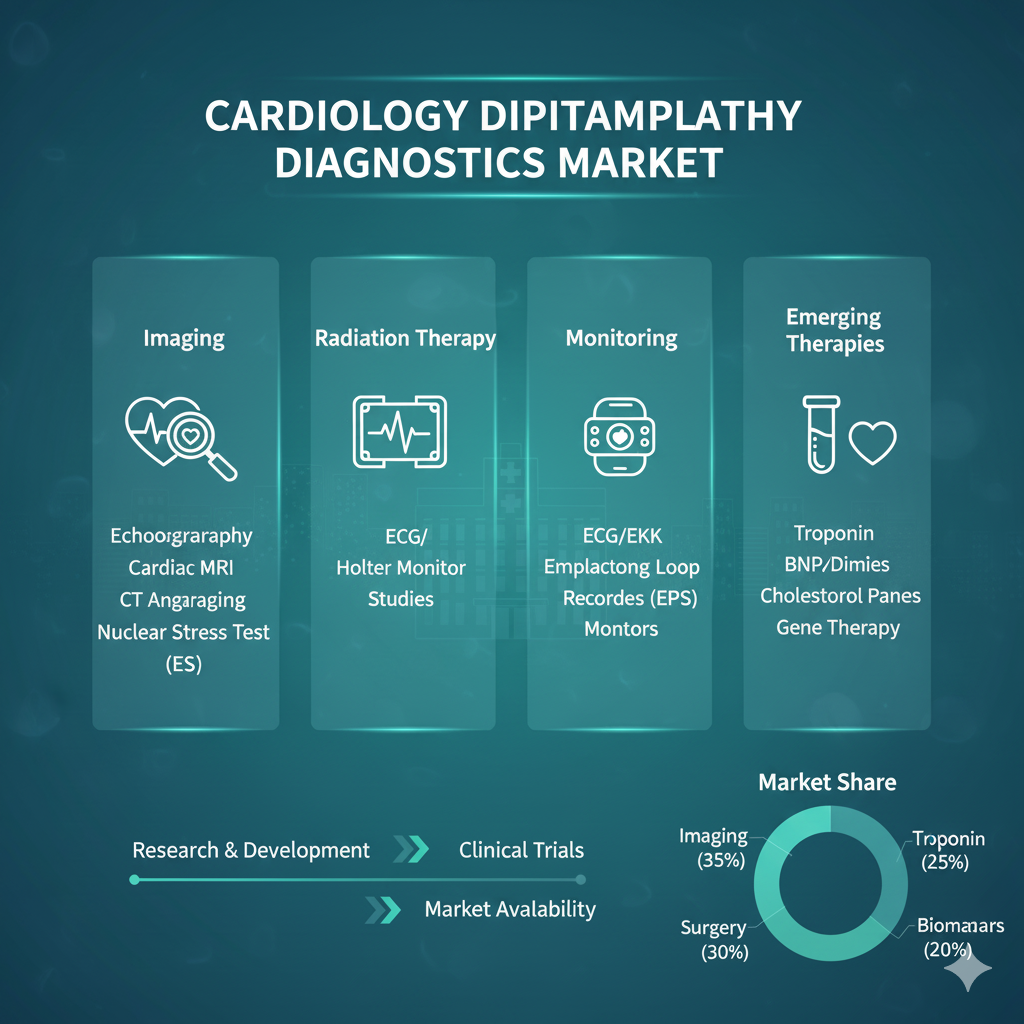

By Product

The market is segmented into electrocardiogram (ECG) systems, Holter monitors, event monitors, implantable loop recorders (ILRs), cardiopulmonary stress testing systems, and others. ECG systems, particularly resting ECG, form the largest and most foundational segment due to their universal use in initial cardiac assessment across all care settings. Holter monitors and event monitors are critical for diagnosing intermittent arrhythmias over 24-48 hours or longer periods. Implantable loop recorders (ILRs) represent a high-growth segment for long-term (years) monitoring of elusive cardiac events. Stress testing systems are essential for evaluating cardiac function under exertion. The trend toward ambulatory and prolonged monitoring is driving growth in wearable and implantable devices.

By Application

Key applications include myocardial infarction (heart attack), arrhythmia, ischemia, hypertrophy, and others. Arrhythmia detection is the dominant application, driven by the high prevalence of conditions like atrial fibrillation and the need for continuous monitoring technologies. Myocardial infarction diagnosis relies heavily on rapid ECG and biomarker testing in emergency settings. Ischemia and hypertrophy assessments are essential for managing coronary artery disease and heart muscle conditions. "Others" include applications in channelopathies and pre-operative screening. The increasing focus on early and precise diagnosis to guide intervention supports demand across all applications.

By End User

Hospitals are the largest end-users, performing the majority of complex diagnostics, emergency care, and surgical planning. Ambulatory surgical centers (ASCs) and specialty clinics (e.g., cardiology clinics) are growing segments for routine monitoring, follow-up care, and elective procedures. Diagnostic imaging centers provide specialized services such as stress testing and advanced imaging. Other end-users include home care settings, supported by the rise of remote patient monitoring technologies. The shift toward decentralized and outpatient care is expanding the role of non-hospital settings in cardiology diagnostics.

Regional Insights

-

North America: Dominates the market due to advanced healthcare infrastructure, high adoption of diagnostic technologies, and significant healthcare expenditure.

-

Europe: Experiences steady growth with strong healthcare systems and increasing focus on preventive cardiology.

-

Asia Pacific: Expected to witness the fastest growth, driven by improving healthcare access, rising awareness, and increasing incidences of cardiovascular diseases.

Key Market Drivers

-

Rising Incidence of Cardiovascular Diseases: The increasing prevalence of heart-related conditions is driving the demand for diagnostic services.

-

Technological Advancements: Innovations in diagnostic tools, such as portable ECG devices and advanced imaging techniques, are enhancing diagnostic accuracy and accessibility.

-

Aging Population: An aging global population is more susceptible to cardiovascular diseases, thereby increasing the need for diagnostic services.

-

Government Initiatives: Supportive healthcare policies and investments in medical infrastructure are facilitating market growth.

Leading Market Players

-

The major global players in the cardiology diagnostics market include GE Healthcare, BPL Medical Technologies, Boston Scientific Corporation, Abbott Laboratories, 3M Company, Koninklijke Philips N.V., Siemens Healthineers, Cardinal Health, Medtronic plc, Hitachi Medical Systems among others.

These companies are focusing on product innovation, strategic partnerships, and expanding their market presence to cater to the growing demand for cardiology diagnostics.

Recent Industry Developments

-

Advancements in Wearable Technology: The development of wearable devices capable of continuous heart monitoring is revolutionizing early detection and management of cardiovascular conditions.

-

Integration of Artificial Intelligence: AI algorithms are being integrated into diagnostic tools to improve accuracy and efficiency in interpreting cardiology diagnostics.

-

Expansion into Emerging Markets: Key players are expanding their presence in emerging markets through collaborations and distribution agreements to tap into the growing demand for diagnostic services.

Conclusion

The cardiology diagnostics market is poised for significant growth through 2031, driven by technological advancements, increasing prevalence of cardiovascular diseases, and supportive healthcare policies. With continuous innovations and expanding access to diagnostic services, the market is set to meet the evolving needs of patients and healthcare providers worldwide.